Why 80% of Seed-Funded Startups Fail to Raise a Series A

The Gap Nobody Warns You About

Getting a seed check feels like a vote of confidence. Someone looked at your deck, your team, your half-baked prototype, and said: I believe in this enough to write you a check. For most founders, that moment carries a kind of emotional weight that’s hard to overstate. It validates the sleepless nights, the awkward pitches at dinner parties, the quiet doubt that maybe this whole thing was a mistake.

And then, somewhere between18 and 24 months later, reality arrives.

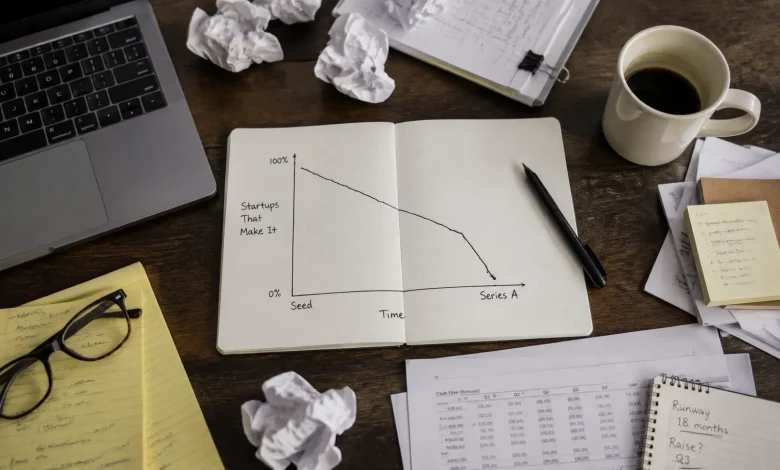

The numbers are unforgiving. Depending on the data source and vintage year, somewhere between 70% and 85% of seed-funded companies never close a Series A. That’s not a rounding error. That’s the rule. The exceptions the companies that actually graduate from seed to Series A are statistically the outliers, not the norm. Yet the entire culture of early-stage startup life is built around the assumption that if you just work hard enough, stay lean enough, and pivot fast enough, you’ll be one of them.

Most won’t be. And the reasons why are almost never what founders expect.

Traction Is Real, But It’s Not Enough

The most common explanation founders give when they fail to raise a Series A is some version of “we just didn’t have enough traction.” That’s technically true in a lot of cases. Series A investors whether it’s a Benchmark, an Andreessen Horowitz, or a mid-tier fund you’ve never heard of are fundamentally running a different calculus than seed investors. At seed, you’re selling potential. At Series A, you’re selling evidence.

But here’s where founders consistently misread the room: they assume that more revenue fixes the problem. It often doesn’t.

A startup doing $400K ARR growing at 8% month-over-month is a more interesting Series A candidate than a startup doing $1.2M ARR growing at 3%. Investors aren’t just looking at the number on the screen they’re looking at what the number implies about the future. Is there a repeatable motion here? Does the unit economics hold up under scrutiny? Is there a world where this becomes a $100M revenue business, or does the market ceiling quietly cap out at $20M?

The traction bar is real, but it’s a proxy measurement for a deeper question: have you demonstrated that you’ve found something that doesn’t just work, but scales?

The Seed Extension Trap

One of the quieter ways seed-stage companies stall out is through a phenomenon that rarely gets discussed openly: the seed extension spiral.

It goes like this. You raised a $1.5M seed. You made progress, but not enough to confidently approach top-tier Series A funds. So a friendly angel or a small fund offers to extend your runway with another $500K. You take it because why wouldn’t you? More runway means more time to hit the numbers, right?

Except that extension round comes with subtle costs that aren’t in the term sheet. Your cap table gets messier. Your story gets harder to tell cleanly. Investors who look at your funding history start asking questions: why has it taken this long? What hasn’t worked? The extension, which felt like a lifeline, has quietly reframed your narrative from “early-stage company on trajectory” to “company that needed more time than expected.”

Some companies do this two or three times. By the third extension, the Series A conversation has effectively been deferred indefinitely. You’re still alive, technically. But you’re no longer on the growth path you’re on the survival path. Those are different roads.

Founder-Market Fit Is Underrated

The startup world talks endlessly about product-market fit. Far less attention goes to founder-market fit the question of whether the specific people running this company are genuinely the right people to scale it.

Series A investors have seen enough companies to develop a finely tuned instinct for this. They’re not just evaluating the business. They’re evaluating whether the founders understand the market as deeply as they claim, whether they’ve developed a perspective that’s earned through real exposure rather than assembled from research reports, and whether they have the personal resilience and adaptability to navigate the brutal middle chapters of building a company.

A founding team that built a B2B SaaS tool for restaurant operators because they spotted a gap in a report is fundamentally different from one where the founder spent six years managing restaurant supply chains before deciding to build software for it. Both might have identical products at seed stage. By Series A, the depth of the latter’s market intuition in their product decisions, their sales motion, their understanding of where competition will come from tends to show up clearly.

This doesn’t mean outsiders can’t succeed. They can. But they have to work harder to demonstrate the equivalent depth, and that demonstration has to show up in the business itself, not just in how well they pitch.

What Investors See That Founders Don’t

There’s an asymmetry of information in Series A fundraising that most founders underestimate. By the time a partner at a decent fund sits across from you physically or on a Zoom call they’ve probably looked at 500 to 1,000 companies that year. They’ve seen your market from six different angles. They’ve met three other teams working on adjacent problems. They’ve tracked two companies in your exact space that raised and subsequently imploded.

Founders walk in thinking the meeting is about conveying information. Investors are actually running a pattern-matching exercise against a very large internal database.

This creates a specific failure mode: founders who over-explain and under-demonstrate. They spend40 minutes on slides and three minutes on the actual business dynamics. They answer every question with confidence, even when the honest answer would be “we’re still figuring that out.” The investors in that room aren’t looking for perfect certainty they’re looking for founders who have a clear-eyed view of where the uncertainty lives and a credible plan for resolving it.

The seed stage rewards storytelling. The Series A stage rewards evidence, combined with the intellectual honesty to contextualize what the evidence does and doesn’t prove.

The Fundraising Strategy Problem

Beyond all the operational and narrative issues, a significant number of seed-stage companies simply run bad fundraising processes and pay for it in ways they never fully diagnose.

Series A fundraising is not a prolonged Series of warm conversations. It’s a compressed, time-sensitive process that needs to be run almost like a campaign. The best outcomes tend to come from founders who have spent months quietly building relationships with target investors before they ever need the money getting on radars, sharing updates, demonstrating momentum in a way that feels organic rather than transactional.

When you finally kick off the formal process, you want as many conversations happening in parallel as possible. You want term sheets to arrive in roughly the same window, because the presence of competition changes investor behavior in ways that are hard to manufacture otherwise. Founders who treat fundraising as a sequential process talk to Firm A, get a no, talk to Firm B almost always end up in a weaker position than founders who’ve engineered genuine optionality.

The ones who get to Series A aren’t just building better products. They’re running better processes, building better relationships, and telling a cleaner story about where the business is and where it’s going. The funding round is almost the last thing to happen everything that matters happened in the 18 months before anyone opened a data room.