The LLC vs. S-Corp Debate: Which Structure Saves You More Money?

Every year, thousands of self-employed Americans reach a tipping point. Revenue climbs, the freelance hustle turns into something that looks and feels like a real business, and suddenly the question that’s been lingering in the background becomes impossible to ignore: should I actually set up a proper business entity? And once you start down that road, you hit the fork almost immediately LLC or S-Corp?

The debate has been rehashed in accounting offices, Reddit threads, and YouTube tutorials for years. But most of the coverage flattens a genuinely nuanced question into a simple answer that doesn’t fit everyone’s situation. The truth is, the “right” choice depends on a set of variables that are specific to you your income level, your tolerance for administrative work, your state of residence, and your long-term plans. Getting it wrong doesn’t mean disaster, but getting it right can mean keeping thousands of dollars that would otherwise flow directly to the IRS.

The Foundation: What Each Structure Actually Is

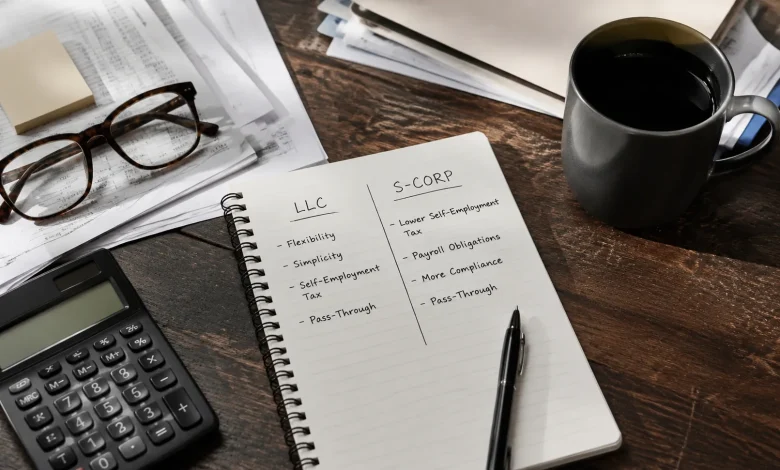

An LLC a limited liability company is fundamentally a legal structure, not a tax designation. When you form an LLC as a single owner, the IRS treats it as a “disregarded entity” by default, which means your business income flows straight through to your personal tax return. You’re still responsible for self-employment tax on every dollar of net profit. That rate sits at 15.3% on the first $176,100 of net earnings in 2025, covering both the employee and employer sides of Social Security and Medicare.

An S-Corp, on the other hand, is a tax election, not a separate legal entity in the same sense. You can elect S-Corp status for an existing LLC or a corporation by filing Form 2553 with the IRS. What changes isn’t the liability protection that stays largely intact but how your income gets taxed. As an S-Corp owner-employee, you split your income into two buckets: a reasonable salary and a distribution. You pay self-employment taxes only on the salary portion. The distributions flow through to your personal return without that 15.3% self-employment tax attached.

That’s the core of the arbitrage. And it’s real.

Running the Numbers: When the Math Actually Favors S-Corp

Say you’re a graphic designer earning $150,000 in net profit annually. As a single-member LLC with default taxation, you owe self-employment tax on the full amount roughly $21,000 before income tax even enters the picture.

Now imagine you make the S-Corp election. Your CPA determines that a reasonable salary for your role is $70,000. You pay yourself that salary, withhold payroll taxes on it, and take the remaining $80,000 as a distribution. Your self-employment tax exposure is now tied to $70,000 instead of $150,000 a difference of roughly $12,000 in tax liability.

That’s a meaningful number. For some business owners, it’s a car payment, a vacation, a few months of health insurance premiums.

But here’s where the math gets more complicated: running payroll isn’t free. You need payroll software or a payroll service, typically running $500to $2,000 per year. You’ll likely need a business bank account set up properly, quarterly payroll tax filings, and at the very least, annual bookkeeping that’s clean enough to support the structure. A good CPA who handles S-Corp returns charges more than one who handles a simple Schedule C often $500 to $1,500 more per year.

Stack those costs against your projected self-employment tax savings, and a clear breakeven point starts to emerge. Most tax professionals put that figure somewhere around $50,000 to $60,000 in annual net profit, though it shifts depending on your state and the administrative setup you already have. Below that threshold, the savings rarely justify the overhead. Above it, the gap widens considerably.

The “Reasonable Salary” Problem

There’s one concept at the center of this entire strategy that deserves more attention than it usually gets: the reasonable salary requirement.

The IRS is not naive. They’re well aware that S-Corp owners have an incentive to pay themselves a salary of $1and take everything else as a distribution. So the rules require that owner-employees receive compensation “comparable to what would be paid for similar services by similar enterprises.” The definition is intentionally vague, which creates both flexibility and risk.

If you run a solo consulting firm and you’d typically bill out at $200 per hour in your market, you can’t justify paying yourself $30,000 a year and calling it reasonable. The IRS has gone after S-Corp owners for exactly this, reclassifying distributions as wages and hitting them with back taxes, interest, and penalties.

Setting your salary correctly requires honest research industry salary surveys, BLS data, comparable job postings and ideally, documentation that shows your reasoning. It’s not complicated, but it is something you need to take seriously. The savings only work if the structure holds up under scrutiny.

State-Level Complications That Most Articles Skip

Federal tax savings are the main event, but state-level rules can quietly erode them.

California, for instance, charges LLCs an annual franchise tax that scales with revenue, and S-Corps face their own set of fees and minimum franchise taxes. The net benefit of the S-Corp election can look different in Sacramento than it does in Austin. Some states don’t recognize S-Corp status at all for state income tax purposes, meaning you get the federal benefit but no corresponding state relief.

New York City adds a general corporation tax on S-Corps operating within the five boroughs. Tennessee taxes certain types of pass-through income in ways that can affect your calculus. These aren’t edge cases they’re real considerations that vary enough to change the optimal answer depending on where you live and work.

This is one reason why generic advice on the internet can only take you so far. A CPA who knows your state’s specific rules is worth the consultation fee before you make any structural decisions.

Timing, Flexibility, and the Long Game

One underappreciated aspect of this choice is the flexibility the LLC structure provides before you elect S-Corp status. You can form your LLC, operate under default taxation while your income is still building, and then make the S-Corp election later typically by March15 of the tax year in which you want the election to take effect, or within75 days of forming a new entity.

That timeline means you’re not forced to commit to the administrative overhead of an S-Corp before it makes financial sense. A lot of freelancers will start as a single-member LLC, grow their revenue over a few years, and then add the S-Corp election once the savings clearly outweigh the costs. It’s a staged approach that lets the structure evolve alongside the business.

There’s also a conversation worth having about exit strategies. If you ever plan to bring on investors or eventually sell the business, S-Corp status comes with restrictions you can have no more than 100 shareholders, all of whom must be U.S. citizens or residents, and only one class of stock is allowed. These constraints rarely matter for solo operators and small service businesses, but if growth is on the horizon in ways that might attract outside capital, the structure you choose now can create friction later.

What Actually Moves the Needle

Strip away the noise, and the decision usually comes down to two things: your net profit level and your appetite for administrative structure.

If you’re clearing $80,000 or more in net profit from self-employment, the S-Corp election deserves a serious look. The self-employment tax savings are real, they compound year over year, and the administrative burden while real is manageable with the right setup. Below that range, the LLC’s simplicity often wins on pure economics.

What doesn’t make sense is choosing a structure based on how it sounds or how sophisticated you want to feel. S-Corps carry a certain cache in entrepreneurial circles, but a solo contractor making $40,000 in net profit who converts to S-Corp status is almost certainly spending more on compliance than they’re saving in taxes.

The best version of this decision isn’t a choice between two fixed options it’s a conversation with a CPA who can model out both scenarios with your actual numbers. Not a general estimate, not a calculator you found online, but a projection built on your specific income, your state, your deductions, and your goals. That conversation, even if it costs a few hundred dollars, will almost always pay for itself.